16 July 2023

Content:

Content:

- Summary

- Two issues when valuing a tech business

- Six historical challenges for investors

- FAANGs: what’s my story in 20 seconds?

- Would I buy Nvidia now?

- Final thoughts

- P.S.: more exciting sectors than tech

Summary

S&P 500 is up 17.8% year-to-date. I am significantly behind the index with a little over 5% gain. Even though I did materially better last year (relative to the broader market), it is still frustrating.

I don’t know your performance, but I know the key factor that drove it - your exposure to the tech sector. The tech sector accounts for 62% of the S&P 500 gain in the first half of 2023, while in May, practically all the gains in the index came from tech.

On the other hand, 40% of the S&P 500 stocks are either flat or down this year.

Congratulations if you are a happy owner of a few exciting tech stocks! You know it better than me. If you do not and feel confused, let me share my thoughts with you.

As a contrarian, I am cautious about the tech sector. I see more exciting opportunities in other, less popular places (I will tell you about them at the end of this post).

The giant tech companies have become so big by now that their future growth will match global GDP at best (single digit). Did I forget to mention that they trade above 30x? Do not expect sustainable returns from further re-rating. The only way for these large businesses to deliver above-average returns is to enter new verticals. The problem is that most of these verticals are not big enough to move the needle. And many are rushing in the same direction, ready to spend billions.

There may be exceptions. Perhaps, Nvidia is in a unique position, as the bulls suggest. It is in a too-hard pile for me.

The small tech companies are in an even more challenging situation. Due to their size, they do not benefit from networking effects, high switching costs, brand loyalty and all other features that define durable competitive advantages.

I don’t know your performance, but I know the key factor that drove it - your exposure to the tech sector. The tech sector accounts for 62% of the S&P 500 gain in the first half of 2023, while in May, practically all the gains in the index came from tech.

On the other hand, 40% of the S&P 500 stocks are either flat or down this year.

Congratulations if you are a happy owner of a few exciting tech stocks! You know it better than me. If you do not and feel confused, let me share my thoughts with you.

As a contrarian, I am cautious about the tech sector. I see more exciting opportunities in other, less popular places (I will tell you about them at the end of this post).

The giant tech companies have become so big by now that their future growth will match global GDP at best (single digit). Did I forget to mention that they trade above 30x? Do not expect sustainable returns from further re-rating. The only way for these large businesses to deliver above-average returns is to enter new verticals. The problem is that most of these verticals are not big enough to move the needle. And many are rushing in the same direction, ready to spend billions.

There may be exceptions. Perhaps, Nvidia is in a unique position, as the bulls suggest. It is in a too-hard pile for me.

The small tech companies are in an even more challenging situation. Due to their size, they do not benefit from networking effects, high switching costs, brand loyalty and all other features that define durable competitive advantages.

Two issues when valuing a tech business

These four factors drive the value of any business:

1) near-term earnings

2) growth

3) life span

4) certainty

Most tech companies score great on the first two points, but problems arise with the last two points. This has been proven time and again in the past. An example from my youth days:

Starting with just 1 million subscribers in 1994, AOL reached 27 million in 2002, achieving a 50% CAGR. But just a decade later, AOL had only 3 million paying US subscribers — remarkable growth but not a long life span.

1) near-term earnings

2) growth

3) life span

4) certainty

Most tech companies score great on the first two points, but problems arise with the last two points. This has been proven time and again in the past. An example from my youth days:

Starting with just 1 million subscribers in 1994, AOL reached 27 million in 2002, achieving a 50% CAGR. But just a decade later, AOL had only 3 million paying US subscribers — remarkable growth but not a long life span.

Six historical challenges for investors

Challenge 1. Time and place matter more than the technology

Imagine a young innovator. He has shown an excellent aptitude for technology from a young age and is especially intrigued by electricity. He is attending classes at a leading Polytechnical College at night while helping his father in his mechanical shop by day.

At 26, he leads the production of the first hybrid car in the world.

The electric car industry is booming, accounting for almost 40% of all cars sold. However, due to the lack of charging stations, such vehicles could not cover long distances and soon lost their appeal.

That gentleman's name is Dr. Ing. Ferdinand Porsche, the founder of one of the world’s best auto brands, who was born 148 years ago.

At 26, he leads the production of the first hybrid car in the world.

The electric car industry is booming, accounting for almost 40% of all cars sold. However, due to the lack of charging stations, such vehicles could not cover long distances and soon lost their appeal.

That gentleman's name is Dr. Ing. Ferdinand Porsche, the founder of one of the world’s best auto brands, who was born 148 years ago.

He was far ahead of his peers in applying scientific breakthroughs to the car industry, yet his hybrid model did not take off due to a lack of supporting infrastructure. He was too early.

Compare his story to Steve Jobs, who put together all the latest technologies in one place under an elegant design and called his product an iPhone. It would not have been possible if telecoms had not covered our planet with towers, touchscreen technology did not exist, as well as many other inventions such as mobile cameras, software, microprocessors and batteries.

Even if you back the most promising technology, you will still lose money unless it hits the market at the right time.

Compare his story to Steve Jobs, who put together all the latest technologies in one place under an elegant design and called his product an iPhone. It would not have been possible if telecoms had not covered our planet with towers, touchscreen technology did not exist, as well as many other inventions such as mobile cameras, software, microprocessors and batteries.

Even if you back the most promising technology, you will still lose money unless it hits the market at the right time.

Challenge 2. The new product is exciting, and this is exactly the problem

New exciting technologies come with alluring promises. Hence, raising capital for companies associated with anything new (Internet in the 1990s, AI in 2020?) is not a problem. But this is precisely what creates the foundation for investors’ misfortunes later on. Too much capital increases competition and ruins sector economics. It also shortens product life cycles.

Can you believe that a hundred years ago, there were about 100 independent car manufacturers in the US?

Other “innovative” sectors did not do much better.

Here is Peter Lynch’s account:

Can you believe that a hundred years ago, there were about 100 independent car manufacturers in the US?

Other “innovative” sectors did not do much better.

Here is Peter Lynch’s account:

“There’s never been a hotter stock than Xerox in the 1960s. Copying was a fabulous industry, and Xerox had control of the entire process. “To Xerox” became a verb, which should have been a positive development. Many analysts thought so. They assumed that Xerox would keep growing to infinity when the stock was selling for $170 a share in 1972. But then the Japanese got into it, IBM got into it, and Eastman Kodak got into it. Soon there were 20 firms that made nice dry copies, as opposed to the original wet ones. Xerox’s share price dropped 84%. Several competitors didn’t fare much better.”

And he continues:

“Remember what happened to disk drives? The experts said that this exciting industry would grow at 52% a year - and they were right, it did. But with 30 or 35 rival companies scrambling on the action, there were no profits.”

From One Up on Wall Street

The book Capital Returns makes a great point that the flow of capital is the most critical factor of future returns in that industry as opposed to the end demand.

The book Capital Returns makes a great point that the flow of capital is the most critical factor of future returns in that industry as opposed to the end demand.

Challenge 3. The right technology, but is it the right company?

It is not enough to identify the pioneer in an industry. History is ripe with examples when a debut product is dwarfed by a late rival. I still remember the days when MySpace was the main social media network, long before Facebook. I also used Yahoo for searching on the Internet many years before Google became the dominant engine.

Alasdair Nairn, the CEO of Edinburgh Partners and chairman of the Templeton Global Equity Group, made this thought-provoking remark on investing in the automobile revolution:

Alasdair Nairn, the CEO of Edinburgh Partners and chairman of the Templeton Global Equity Group, made this thought-provoking remark on investing in the automobile revolution:

“If by chance you had been able to identify the genius of Henry Ford at an early stage, it would have been important to wait until he had been bankrupt twice before investing in his third venture, the Ford Motor Company. Or, in the case of General Motors, you would have needed to twice avoid the acquisitive excesses of Durant. In the same way the investor would have had to know that the two existing technologies, electricity and steam, would fail to maintain their progress and be overtaken by the internal combustion engine.”

From Engines That Move Markets: Technology Investing from Railroads to the Internet and Beyond

Besides, real innovators are often driven by non-financial interests. Listen to what the world’s most prominent innovator, Thomas Edison, once said:

Besides, real innovators are often driven by non-financial interests. Listen to what the world’s most prominent innovator, Thomas Edison, once said:

“My main purpose in life is to make enough money to create ever more inventions.”

Still, he did better financially than Nikola Tesla, who spent virtually every cent he had on new experiments and always needed more funding. In the end, he died broke.

Measuring the innovative process using traditional accounting is impossible. For accountants, a failed experiment is a cost that reduces profitability. For scientists, a failed experiment is one from which they learn nothing and cannot arrive at a conclusion about their hypothesis.

Measuring the innovative process using traditional accounting is impossible. For accountants, a failed experiment is a cost that reduces profitability. For scientists, a failed experiment is one from which they learn nothing and cannot arrive at a conclusion about their hypothesis.

Challenge 4. Many discoveries come from unexpected places

There are dozens of cases of technologies being used in entirely unexpected ways.

For example, when radio was initially developed, its primary purpose was to provide long-distance wireless communication, primarily for maritime and military purposes across vast distances, replacing telegraphs that relied on wires.

However, as technology advanced and broadcasting capabilities improved, radio quickly became a medium for entertainment and news dissemination.

Other “unexpected” inventions include X-rays, Lasers, MRI scans, Radar, Nuclear energy, Microwave ovens and many more.

The history suggests that the thread for a tech company may not be from its direct peer but an utterly random company. Imagine going for a gunfight in a dark room, not knowing how many opponents you face.

For example, when radio was initially developed, its primary purpose was to provide long-distance wireless communication, primarily for maritime and military purposes across vast distances, replacing telegraphs that relied on wires.

However, as technology advanced and broadcasting capabilities improved, radio quickly became a medium for entertainment and news dissemination.

Other “unexpected” inventions include X-rays, Lasers, MRI scans, Radar, Nuclear energy, Microwave ovens and many more.

The history suggests that the thread for a tech company may not be from its direct peer but an utterly random company. Imagine going for a gunfight in a dark room, not knowing how many opponents you face.

Challenge 5. Great technology, but fickle customers

Most technologies emerge as cheap and more convenient alternatives to existing solutions (e.g. automobiles replacing horse-drawn carriages). But they rarely grow to become big brands. Lacking the support of loyal customers, such companies fail to raise prices and continue to struggle with low margins.

Most of the hundred auto companies in the US that operated in the 1920s went bust. Railroads, electric utilities, airlines and other “revolutionary” services followed a similar pattern.

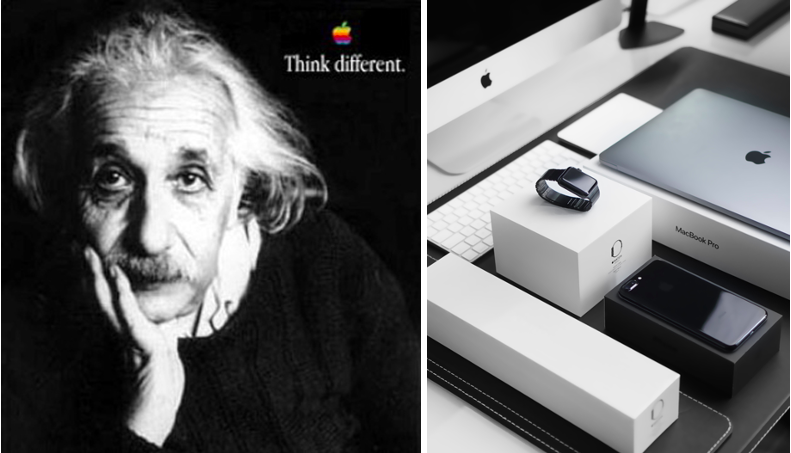

Apple is the most prominent exception. Do you remember its “Think Different” ad campaign, which referred to images of Einstein, Ali, Picasso, Hitchcock, Martin Luther King, Pablo Picasso and others? Its elegant design and other unique features allowed it to win over a billion loyal customers (at least for now).

Most of the hundred auto companies in the US that operated in the 1920s went bust. Railroads, electric utilities, airlines and other “revolutionary” services followed a similar pattern.

Apple is the most prominent exception. Do you remember its “Think Different” ad campaign, which referred to images of Einstein, Ali, Picasso, Hitchcock, Martin Luther King, Pablo Picasso and others? Its elegant design and other unique features allowed it to win over a billion loyal customers (at least for now).

Challenge 6. Technology has to be young, which is against Lindy’s law

Tech companies, by default, fail the Lindy test. The Lindy effect predicts that the time an object (non-perishable) will exist in the future corresponds with the time it has existed until now. For example, books published centuries ago are likely to be read for several centuries in the future. On the other hand, a Manhattan musical that has been on stage for just half a year will likely remain popular for another six months.

Technology has to be new to remain popular and appealing. No one wants to drive a car with a carburettor, manual transmission, no display, old radio and doors that you cannot open remotely. Not only this increases the need to keep R&D spending high, but it also adds to uncertainty as there is no crystal ball to say whether a new project will lead to another successful innovation.

Not surprisingly, perhaps, that one of the most successful tech founders, Jeff Bezos, has the following secret for staying relevant in the fast-changing industry:

Technology has to be new to remain popular and appealing. No one wants to drive a car with a carburettor, manual transmission, no display, old radio and doors that you cannot open remotely. Not only this increases the need to keep R&D spending high, but it also adds to uncertainty as there is no crystal ball to say whether a new project will lead to another successful innovation.

Not surprisingly, perhaps, that one of the most successful tech founders, Jeff Bezos, has the following secret for staying relevant in the fast-changing industry:

“I very frequently get the question: 'What's going to change in the next 10 years?' And that is a very interesting question; it's a very common one. I almost never get the question: 'What's not going to change in the next 10 years?' And I submit to you that that second question is actually the more important of the two - because you can build a business strategy around the things that are stable in time. ... In our retail business, we know that customers want low prices, and I know that's going to be true 10 years from now. They want fast delivery; they want a vast selection. It's impossible to imagine a future 10 years from now where a customer comes up and says, 'Jeff, I love Amazon; I just wish the prices were a little higher.’”

— Jeff Bezos, founder of Amazon

You can reasonably ask: “What about Microsoft or Apple? Did not the best returns for their shareholders come from holding their shares from the first day until now, through thin and thick?”

I would say they are probably an exception. It is never obvious at the IPO that a particular technology will become the global standard in its sector. At least statistical chances for that are meagre.

But it is worth paying attention to signs when it is about to happen. Size and scale are important. Once a product has many users, see if they face high switching costs, if the product benefits from the network effects, if customers don’t have a better alternative, or if you personally struggle to live without a particular product.

These are the reasons I previously owned Apple, Google and Amazon.

I would say they are probably an exception. It is never obvious at the IPO that a particular technology will become the global standard in its sector. At least statistical chances for that are meagre.

But it is worth paying attention to signs when it is about to happen. Size and scale are important. Once a product has many users, see if they face high switching costs, if the product benefits from the network effects, if customers don’t have a better alternative, or if you personally struggle to live without a particular product.

These are the reasons I previously owned Apple, Google and Amazon.

Would I buy Nvidia now?

Instead of answering this question, let me quote Peter Lynch, the legendary portfolio manager at Fidelity, who achieved 29.2% annual returns while S&P 500 delivered 13.2% annually during the same period.

“If I could avoid a single stock, it would be the hottest stock in the hottest industry, the one that gets the most favourable publicity, the one that every investor hears about in the carpool or on the commuter train - and succumbing to the social pressure, often buys.”

Final thoughts

I don’t want to leave you with the idea that the technology sector is uninvestable. It is crucial to be aware of what makes this sector more challenging to invest in (specifically, longevity and certainty) and be aware of historical patterns. Tech companies could be fantastic investments if the price is low enough or the business is gaining critical scale benefiting from network effects or rising brand loyalty. With low distribution costs and high fixed costs, incremental sales can come with extraordinary margins fuelling the overall earnings growth of the company.

To conclude this post, I will quote the dean of value investing, Ben Graham. I am especially keen to use Graham’s words because so many people misunderstand him. He did not advocate buying cheap stocks as many novice investors believe (check my review of The Intelligent Investor. His writing is much more nuanced. Each time I read Intelligent Investor, I discover many new ideas.

To conclude this post, I will quote the dean of value investing, Ben Graham. I am especially keen to use Graham’s words because so many people misunderstand him. He did not advocate buying cheap stocks as many novice investors believe (check my review of The Intelligent Investor. His writing is much more nuanced. Each time I read Intelligent Investor, I discover many new ideas.

“More so than in the past, the progress or retrogression of the typical company in the coming decade may depend on its relation to new products and new processes, which the analyst may have a chance to study and evaluate in advance. Thus there is doubtless a promising area for effective work by the analyst, based on field trips, interviews with research men, and on intensive technological investigation on his own. There are hazards connected with investment conclusions derived chiefly from such glimpses into the future, and not supported by presently demonstrable value. Yet there are perhaps equal hazards in sticking closely to the limits of value set by sober calculations resting on actual results. The investor cannot have it both ways. He can be imaginative and play for the big profits that are the reward for vision proved sound by the event; but then he must run a substantial risk of major or minor miscalculation. Or he can be conservative, and refuse to pay more than a minor premium for possibilities as vet unproved; but in that case, he must be prepared for the later contemplation of golden opportunities foregone.“

- The Intelligent Investor by Benjamin Graham

P.S.: more exciting sectors than tech

Europe looks like a great hunting ground. Broad indices have historically lagged the US market, but this is not the full picture. There are many under-researched companies below the radar of large investors here. Many are also run by their founders or founding families, strengthening the alignment of interests and leading to a more long-term focus. Some businesses have been in operation for a hundred years and have been tested during the worst times before.

I started spending more time on natural resources recently, particularly energy (for personal investing opportunities). There is a much stronger supply discipline, while demand remains robust at least until 2030. After the initial rally in 2022, many stocks are down 20-50%.

The US market below the $10bn mark is always interesting. Not being physically there, I may not have the real edge. But it doesn’t stop me from occasionally looking for exciting businesses there.

If you find this article interesting, subscribe to my Newsletter to keep up with new ideas I publish regularly. It would be great to hear your thoughts or questions on the tech sector.

I started spending more time on natural resources recently, particularly energy (for personal investing opportunities). There is a much stronger supply discipline, while demand remains robust at least until 2030. After the initial rally in 2022, many stocks are down 20-50%.

The US market below the $10bn mark is always interesting. Not being physically there, I may not have the real edge. But it doesn’t stop me from occasionally looking for exciting businesses there.

If you find this article interesting, subscribe to my Newsletter to keep up with new ideas I publish regularly. It would be great to hear your thoughts or questions on the tech sector.