Topics I will briefly cover today:

- Stock ideas I am working on

- Meta - too-hard pile

- Alibaba

- I am presenting at the London Value Investing Club on 16 Nov 2022

Stock ideas I am working on

While many market commentators are pointing out that the next decade may be miserable for investors with flat returns and high volatility, it is essential to focus on the bright side. The biggest issue of the past decade was the rise of passive money which essentially bought stocks that were going up, contributing to expanding valuation multiples with little correlation to the fundamentals. Concentration and overcrowded situations were big issues. Global performance was primarily driven by the US market, with EM stocks, for example, living through ‘a lost decade’ (despite the continued growth of their economies).

So while a 300%+ gain in S&P from 2009 by January 2022 may look incredible, many investors missed this unless they held a broad US market index all the time. Even if you invested in the US alone but picked a portfolio of 20-30 stocks and did not have enough of the Tech giants (e.g. Amazon, Alphabet, Microsoft) - you would severely underperform.

Going forward, things may be different with more opportunities for international companies, more fundamental drivers and opportunities for great capital allocators (like Berkshire Hathaway) to take advantage of emerging dislocations.

Here is the list of ideas that are on my watch list:

- Kering - a luxury goods business trading at c. 15x PE with sales growing at 10-20%, solid margins and FCF. The luxury goods market remains fragmented; pricing power is strong almost by default. Most companies are run by founders with long-term thinking. Before 2022, Kering was trading at 25-30x PE. The market has been concerned by high exposure to a single brand (Gucci) and China. I have done some preliminary research on Gucci and feel relatively comfortable with the brand’s quality.

- Volkswagen - the company has a market cap of about €79bn and a net cash position of €24bn (in the Automotive division excluding the net cash in Porsche AG). It has recently sold a 12.5% stake in Porsche AG for €9bn at IPO. The market cap of Porsche AG is now €91bn. So the current 87.5% interest in Porsche AG that VW continues to hold is worth €80bn. Moreover, VW has agreed to sell 25% of ordinary shares in Porsche AG (12.5% economic interest) to Porsche SE, a company controlled by the Porsche and Piech families, which owns 53.3% of voting rights in VW for €10bn by early 2023. VW will pay a special dividend of €19.06/share (based on 49% proceeds from the Porsche AG IPO) in early January 2023. So if you make all the adjustments, you get the value of VW’s business other than Porsche at a negative price. Other businesses include brands like VW, Audi, Bentley, Bugatti, Lamborghini, Ducati, Skoda, commercial vehicles etc.

- NVR - one of the leading home builders in the US with a capital-light model (instead of freezing its capital in a large land bank, the company relies on call options which it utilises only if there is enough demand for new homes to build). The company has been an excellent buyback machine reducing its share count by about a third since 2010 (almost 10% in the past 12 months). It has a market cap of approximately $13.4bn and trades on a PE of 9x (although earnings will likely decline due to higher interest rates and weaker house prices in the near term).

- Warner Brothers Discovery - this is a company that was created through a merger of Discovery with Warner Brothers. The main bet here would be on management - the CEO, David Zaclav, and a key shareholder - John Malone. The stock has been hammered recently, trading at multi-year lows. The critical question is to what extent the recent issues are temporary rather than structural and what is the normalised profitability and growth potential.

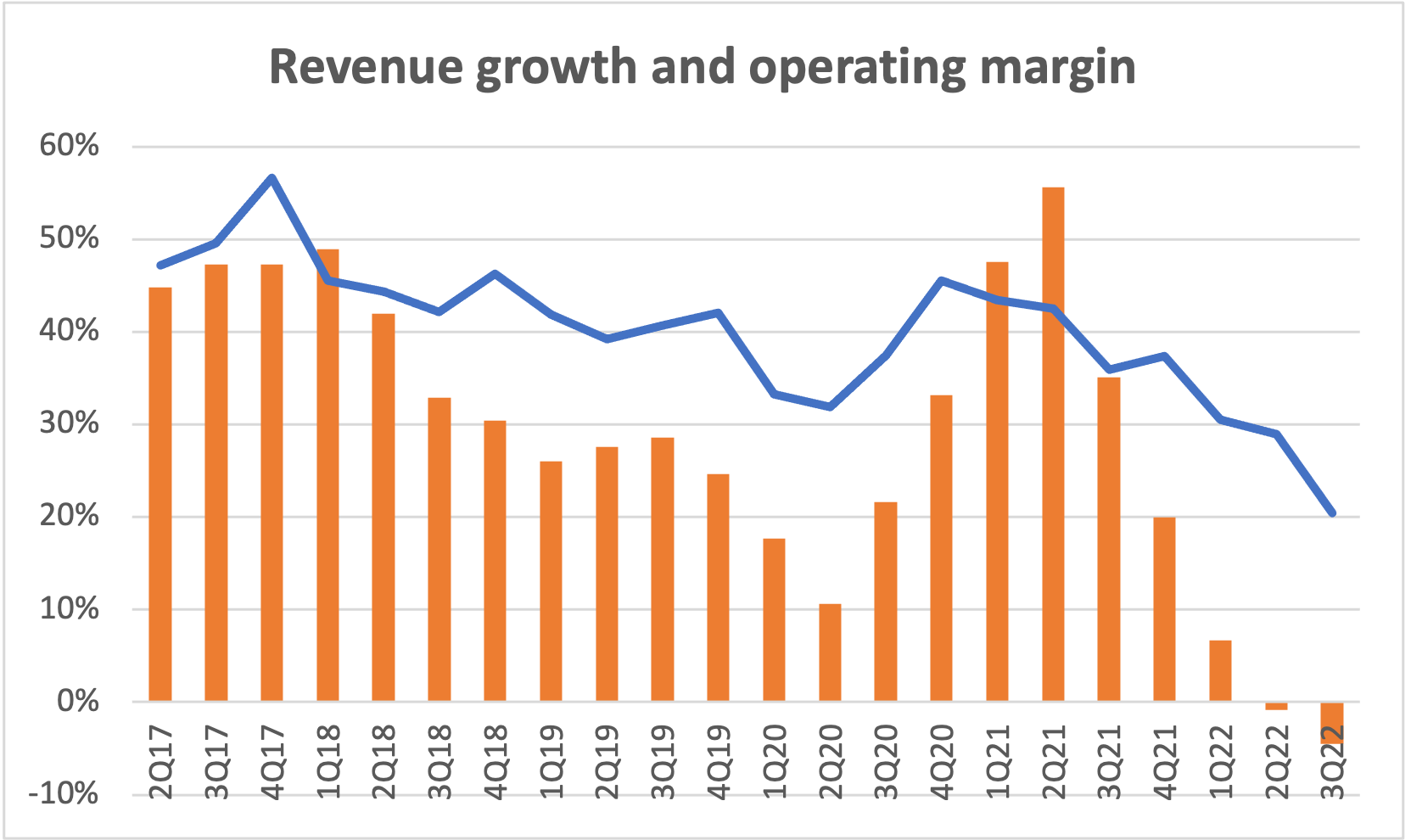

- Adidas - the stock has also collapsed. The main idea is that it is still a consumer franchise brand with better-than-average margins. I need to do more work on the financial performance and operational issues, but the share price chart alone is a strong signal to take a deeper look.

Meta - too-hard pile

My main concern is that the core social media platform (still the biggest in the world) faces much stronger competition from new players like TikTok. Apple’s tracking policy changes also made advertising on the Meta platform less appealing to merchandisers. Will it remain the most popular social network 10 years from now? And what would it take to stay in the top position (in terms of R&D and marketing expenses)? Will it continue to pour billions into the Metaverse, which may or may not be successful?

I have written some further thoughts on Meta here.

Alibaba

I have been thinking about Alibaba a lot recently, whether I made a mistake buying it last year and if I should sell it now. I am inclined to exit because I cannot confidently answer the vital question: Is China investable? The business risks in autocratic regimes are much higher than they may first appear. How sure am I that the shares will continue to be listed? That China will not try to take over Taiwan? That geopolitical tensions will not lead to more sanctions on China and dent its economic growth potential?

I am also finishing my fundamental analysis of Alibaba to see what is the potential upside without such risks. This should help in understanding what has been priced into the stock so far.

I will share my findings shortly.

I am presenting at the London Value Investing Club on 16 Nov 2022

I was invited to speak in front of a small audience on 16 November in London along with two other speakers. The event is primarily for retail investors who are enthusiastic about learning and sharing their views on investing. If you are interested in attending, you can register here.

I think it is a great way of learning and making new friends. If you are interested to meet in a similar format later, just drop me an email (ideas at hiddenvaluegems.com).

Did you find this article useful? If you want to read my next article right when it comes out, please subscribe to my email list.