1 July 2024

What is MSIL about?

This is a short message for new members. I screen many ideas during the month and highlight a few (usually four) that look particularly interesting at the end of each month. There are five criteria that I use to find new ideas:

P.S.: An ideal case would be to find a company that stands out in all five parameters. In reality, there are many exceptions (e.g. Amazon was a low-return business valued at a very high P/E for many years).

P.P.S.: The stocks that appear in MSIL are not automatic buys. MSIL is just the first step in the research process. Usually, a business is cheap because there are two or three issues that put pressure on long-term profits or growth. I focus on those several critical drivers during further research before making the final decision.

- Business Quality: unique product, durable competitive advantage, network effects, high switching costs, barriers to entry, economy of scale.

- Financial performance: strong margins, good growth, high return on capital, high cash conversion

- Low leverage: low debt, preferably net cash position.

- Management with skin in the game: high share ownership by management, preferably founder-led, insider buys, long-term focus, good capital allocation skills.

- Attractive valuation.

P.S.: An ideal case would be to find a company that stands out in all five parameters. In reality, there are many exceptions (e.g. Amazon was a low-return business valued at a very high P/E for many years).

P.P.S.: The stocks that appear in MSIL are not automatic buys. MSIL is just the first step in the research process. Usually, a business is cheap because there are two or three issues that put pressure on long-term profits or growth. I focus on those several critical drivers during further research before making the final decision.

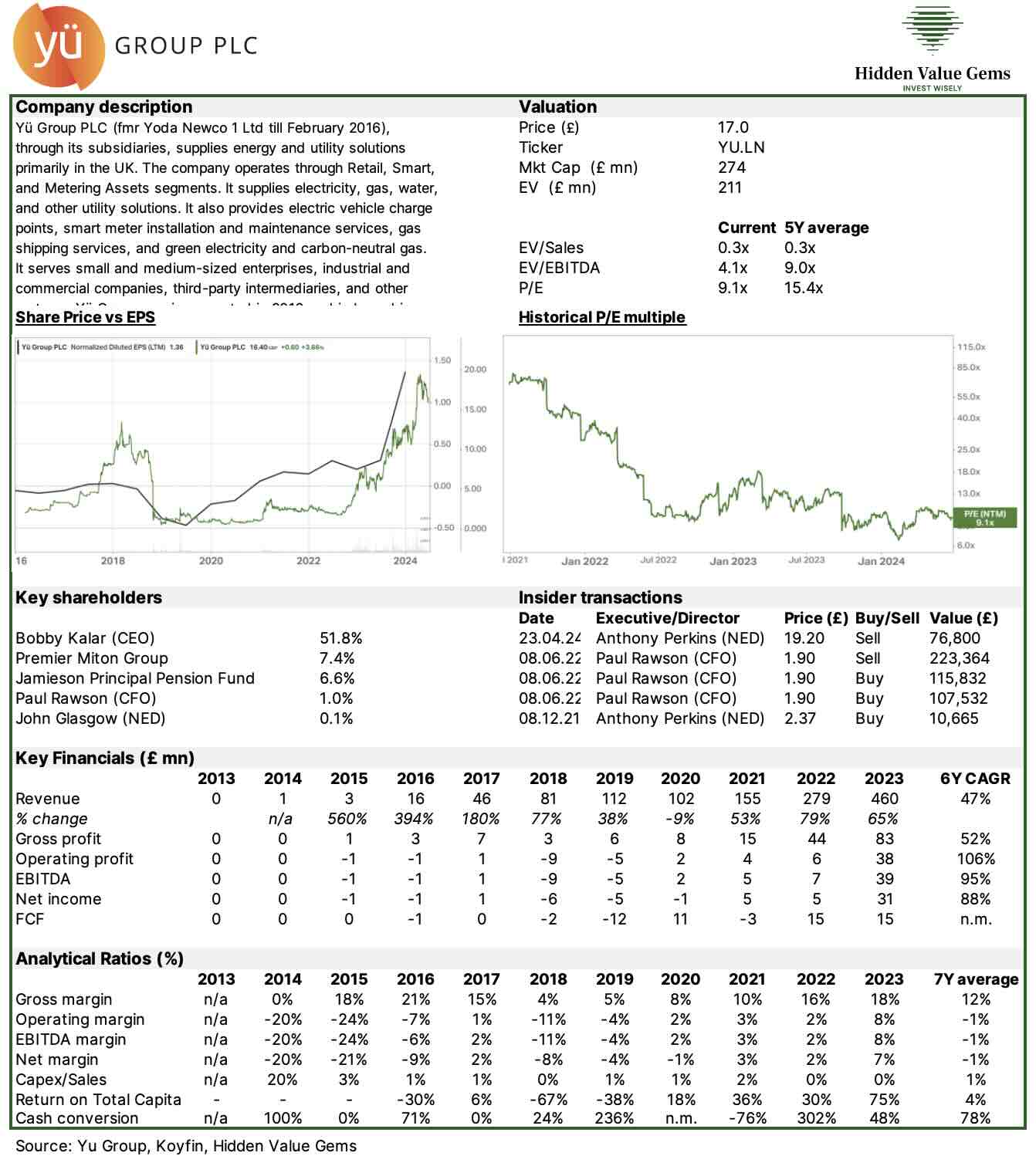

Yu Energy

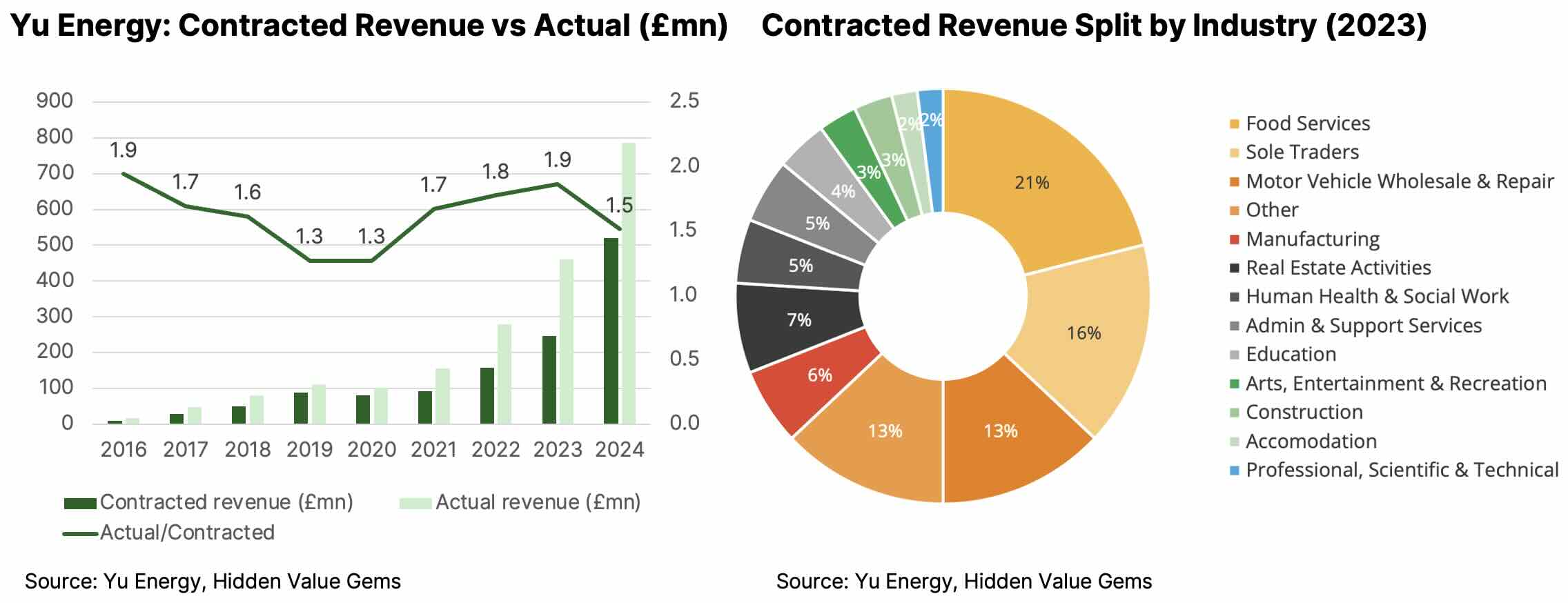

I recently ran a Deep Value screen for UK stocks. One company looked particularly interesting because of its spectacular growth rate and cheap valuation. Yu Energy has delivered 47% compound annual revenue growth in the past six years and is trading at a forward P/E of 9.1x. Adjusted for the net cash position, the stock is at 6.4x.

Yu Energy is a challenger energy supplier in the UK B2B market, focusing on SMEs with an overall market share of c. 1.5%. The company is led by its founder / CEO, Bobby Kalar, the controlling shareholder with a 51.8% interest. The company has a net cash position of £81.9mn, which accounts for 30% of the market cap.

Yu Energy is a challenger energy supplier in the UK B2B market, focusing on SMEs with an overall market share of c. 1.5%. The company is led by its founder / CEO, Bobby Kalar, the controlling shareholder with a 51.8% interest. The company has a net cash position of £81.9mn, which accounts for 30% of the market cap.

Quality product & business

While energy supply may seem like a commodity business with no opportunity for differentiation and excess returns, the reality is somewhat different.

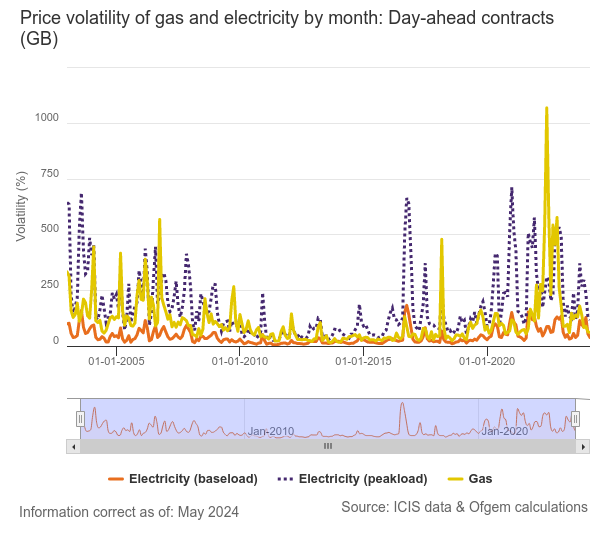

Firstly, electricity and gas prices are highly cyclical during the year and even within 24 hours.

Firstly, electricity and gas prices are highly cyclical during the year and even within 24 hours.

A private business does not have the time and resources to buy energy on the wholesale market at the best price. So, a supplier who can purchase the power on the market would already deliver value. For the customer, the extra benefits come from smoothing out the price volatility, providing a customer with a more predictable and stable expense item. A business can have better visibility, which is critical for planning and budgeting.

However, what differentiates Yu from the incumbent players is the quality of its customer service. This includes transparent and regular billing, easy access (online or by phone) and attractive prices. I have researched what SME customers said about their utility providers, and it seems that the two main points of pain are wrong bills and poor customer service (‘no one answers the phone’, ‘unable to explain the charge’).

I can imagine a business with £300k revenues and a 5% margin (£15k) that gets an extra £2k utility charge (c. 15% hit to the bottom line). In some cases, waiting a few months for a refund can be a material cash flow factor.

Yu Energy benefits from the vision of its founder, who ran a small business before (care homes) and experienced the challenges of dealing with incumbent utilities. He set up Yu Energy to solve those problems for SMEs.

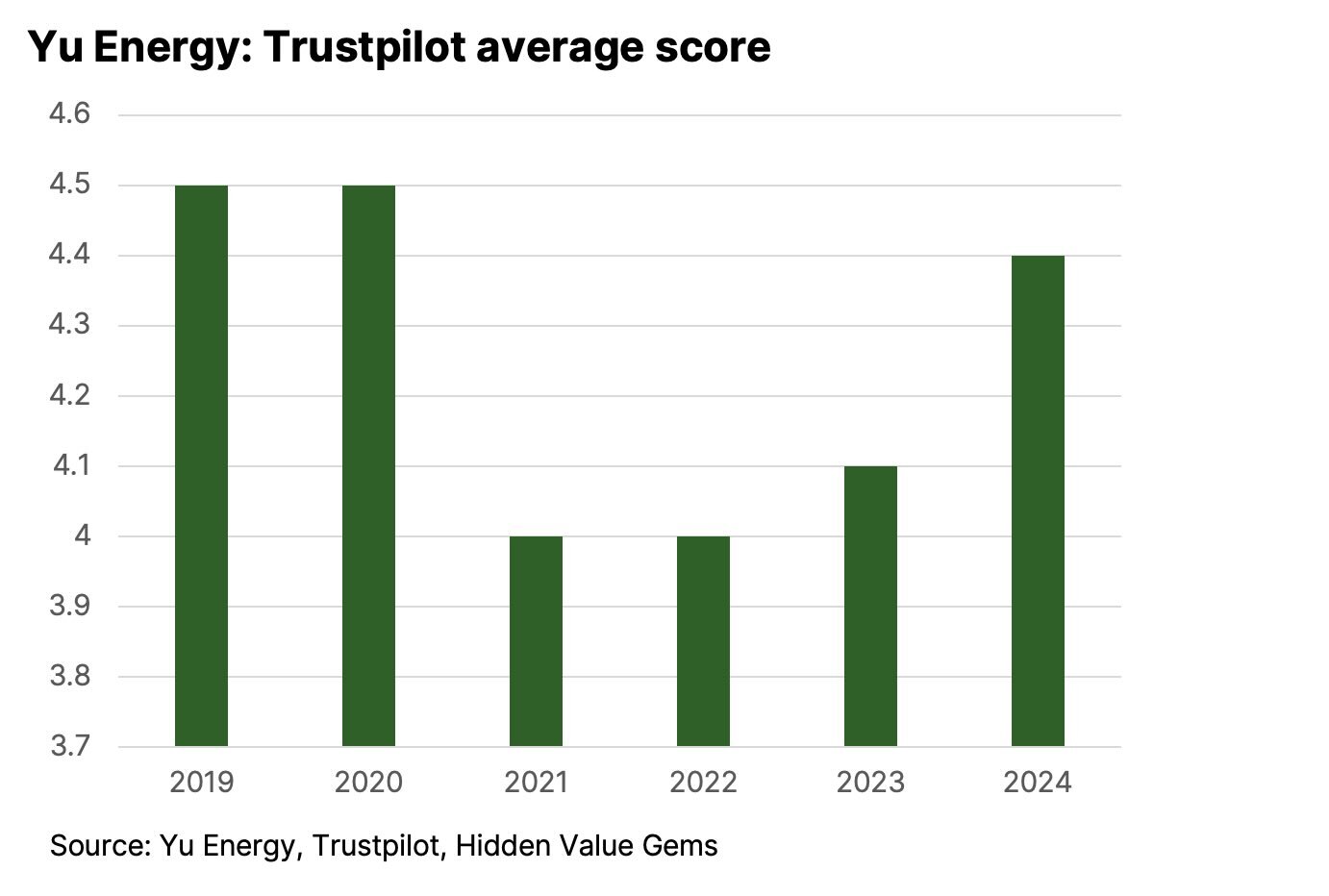

The quality of Yu’s service can be tracked via its high Trustpilot rating. Customer reviews worsened in 2021-22, as there was a general period of disappointment with high prices. But the score has been improving since.

However, what differentiates Yu from the incumbent players is the quality of its customer service. This includes transparent and regular billing, easy access (online or by phone) and attractive prices. I have researched what SME customers said about their utility providers, and it seems that the two main points of pain are wrong bills and poor customer service (‘no one answers the phone’, ‘unable to explain the charge’).

I can imagine a business with £300k revenues and a 5% margin (£15k) that gets an extra £2k utility charge (c. 15% hit to the bottom line). In some cases, waiting a few months for a refund can be a material cash flow factor.

Yu Energy benefits from the vision of its founder, who ran a small business before (care homes) and experienced the challenges of dealing with incumbent utilities. He set up Yu Energy to solve those problems for SMEs.

The quality of Yu’s service can be tracked via its high Trustpilot rating. Customer reviews worsened in 2021-22, as there was a general period of disappointment with high prices. But the score has been improving since.

Barriers to entry

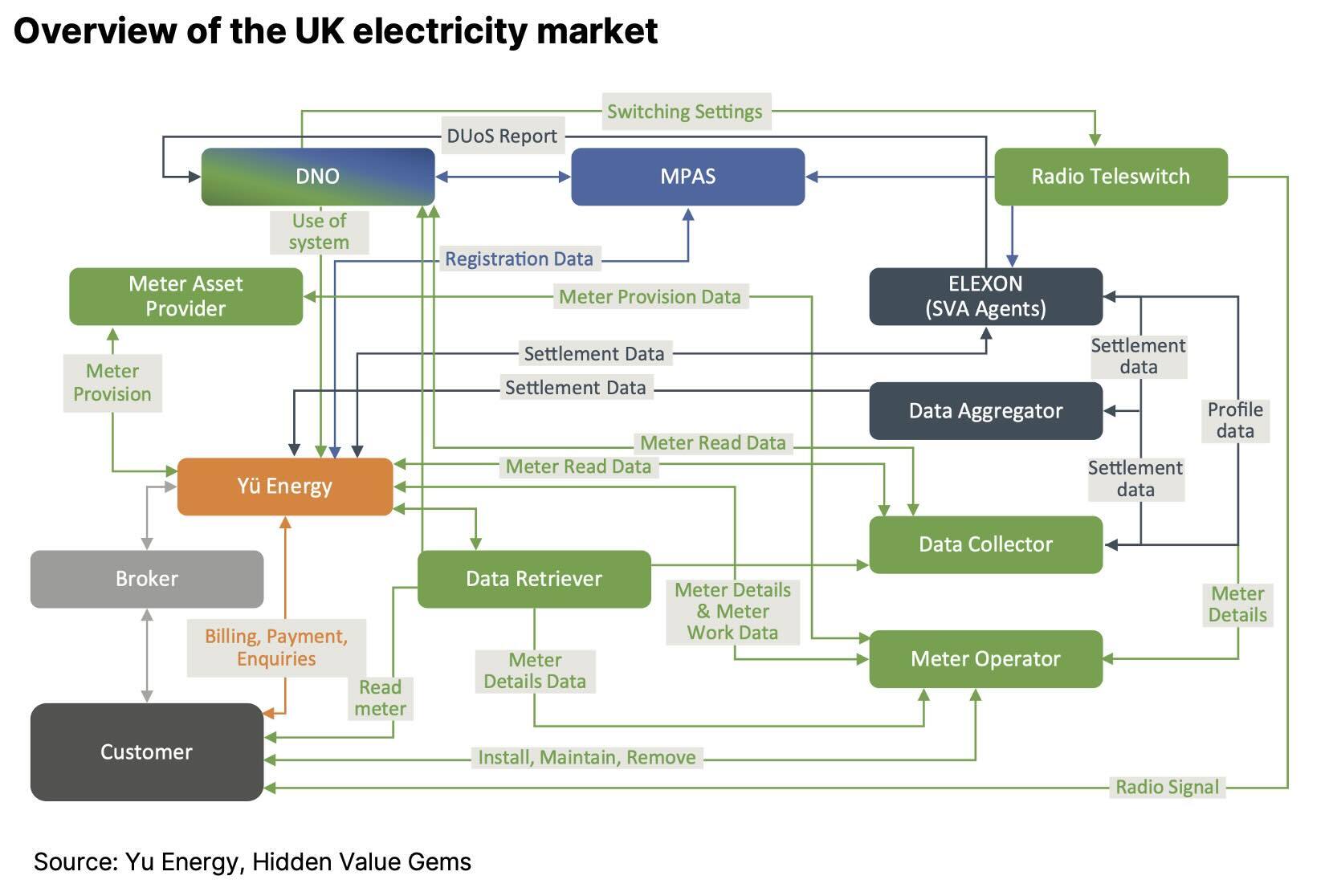

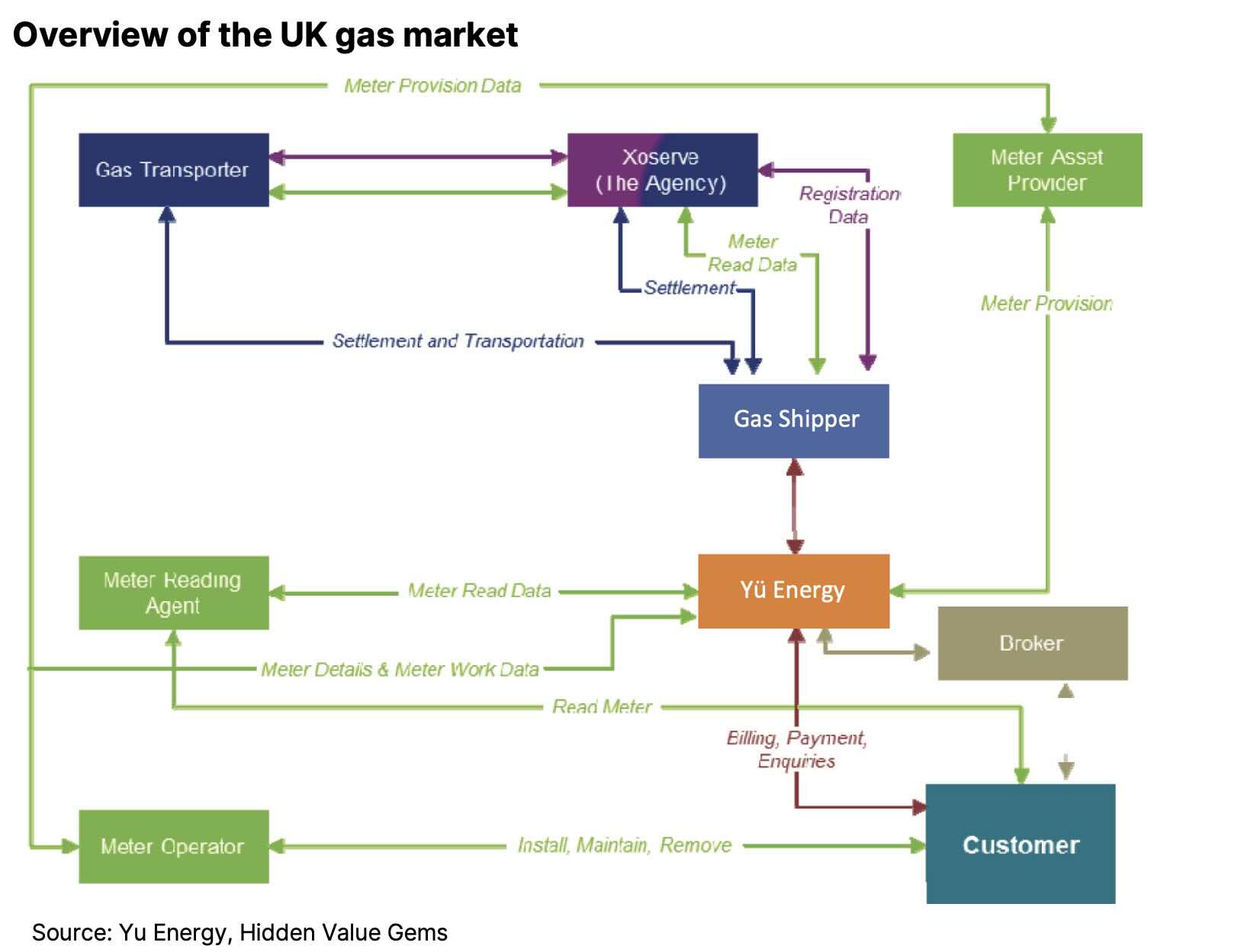

Despite a seemingly simple product (buying energy on the wholesale market and selling it to end customers), the actual business depends on dealing with many counterparties and the regulator. Obtaining a supplier license is a complex process: an applicant must meet several conditions and overcome a lengthy process.

Below are two simplified charts of the UK gas and electricity markets. The graphs are not up to date as Yu has started to own and install its own meters, but they provide a good general idea.

Below are two simplified charts of the UK gas and electricity markets. The graphs are not up to date as Yu has started to own and install its own meters, but they provide a good general idea.

Successfully passed the 'Energy crisis' test

The true strength of the business usually becomes evident during a crisis. It is a great signal to me that during the 2021-2022 'energy crisis,' Yu was buying other suppliers who could not meet their obligations and faced bankruptcy. Specifically, it was appointed by Ofgem (UK regulator) as Supplier of Last Resort (SoLR) for Ampower UK (Nov 2021), Whoop Energy, and Xcel Power (Feb 2022).

Gaining market share

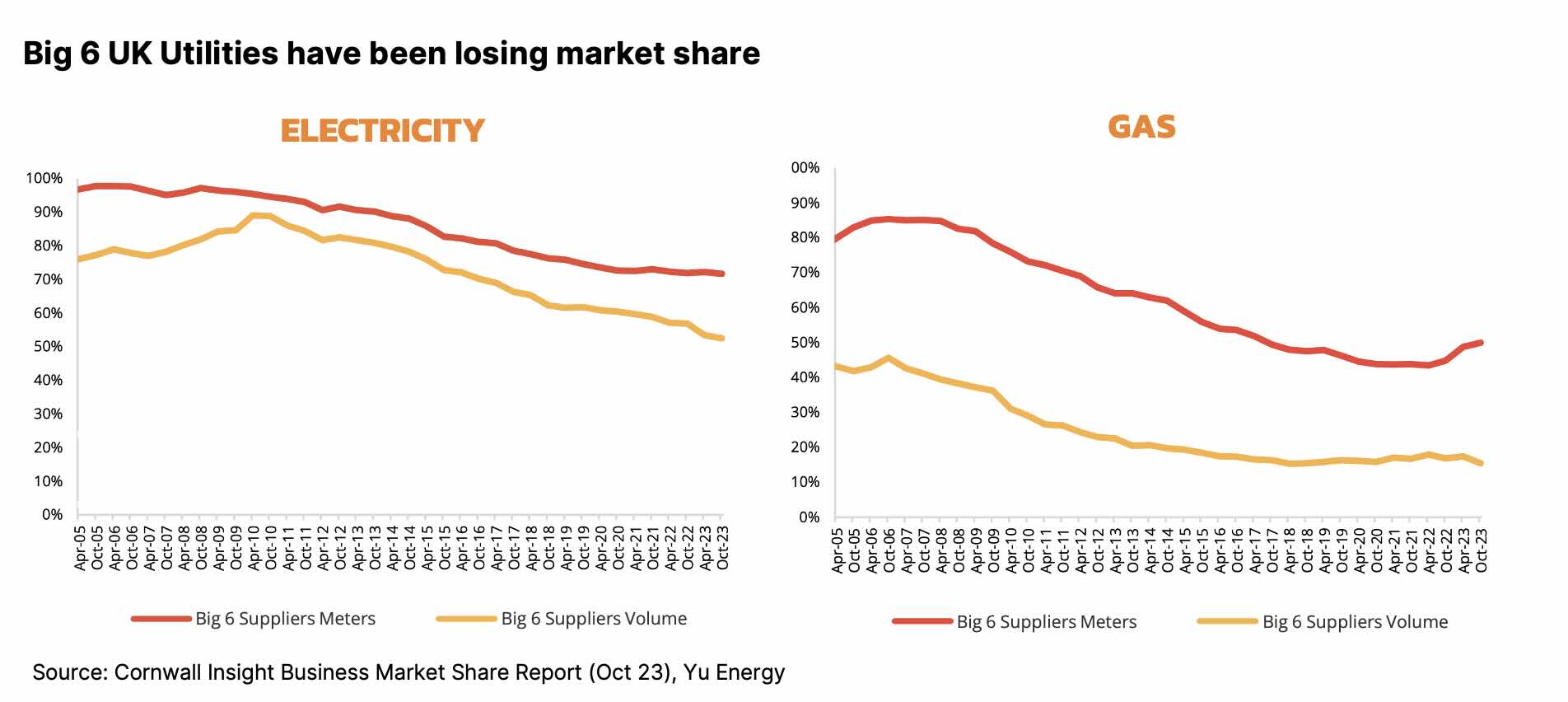

Yu Energy started with zero market share in 2013. It had gained 0.9% share by 2021 and 1.4% in 2023. At the same time, the Big 6 utilities have been losing market shares as a sign of poor customer service, especially in the SME segment. Yu is now the 13th largest energy supplier out of 50 B2B players.

Strong revenue visibility

Yu's business model benefits from the long-term nature of its contracts, which last over 20 months on average. This gives the company visibility over future revenue, as it sells power at fixed rates and has a good understanding of its customers' typical energy use. It can then buy the energy it will have to supply on the wholesale market, hedging the price. This operation requires a strong balance sheet, so not every start-up can afford this.

Such contracts also support improving margins and are fully reflected in the financials with a delay, usually in the following 1-2 years.

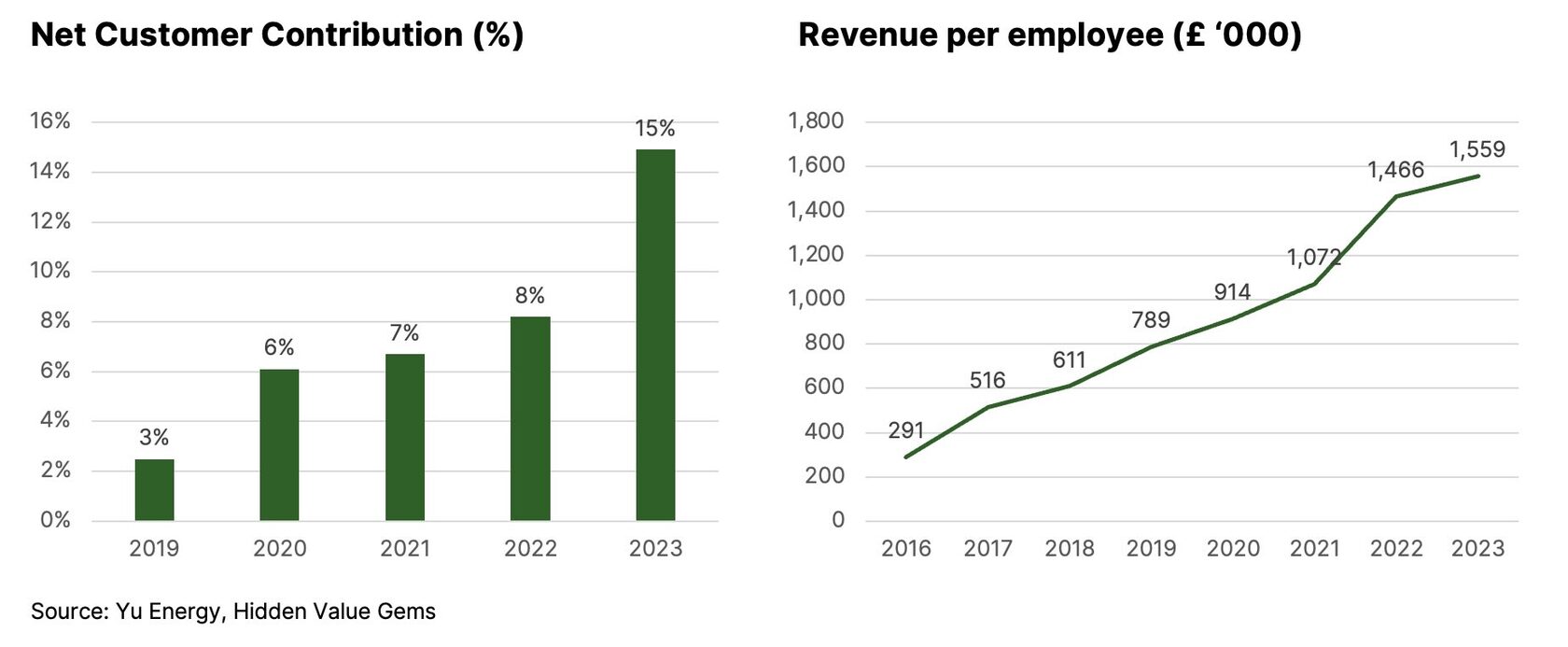

The company has considerably reduced its exposure to weaker customers, with overdue receivables falling to just 4 days. Installing more smart meters and providing fully digital customer communication options is one of the reasons.

Growing in new segments

Over time, the company has diversified from being just a gas and electricity supplier by adding new business lines such as installation and asset management of smart meters, installation of EV charges, and supply of water.

The smart metering business represents an interesting opportunity as the company is paid a fixed annual fee for installing the meter onto the customer’s premises. The contracts usually run for 15 years, and the price is linked to inflation. Yu owned 4.1k and installed 8.5k smart meters by the end of 2023 and plans to grow it to 25k during 2024. This should boost fees to c. £1mn annual fee (growing annually with inflation).

The market potential for further growth is very strong, given that 1.2 million customers still need to install smart meters (Yu will account for just 2.4% of the market by the end of 2024).

The smart metering business represents an interesting opportunity as the company is paid a fixed annual fee for installing the meter onto the customer’s premises. The contracts usually run for 15 years, and the price is linked to inflation. Yu owned 4.1k and installed 8.5k smart meters by the end of 2023 and plans to grow it to 25k during 2024. This should boost fees to c. £1mn annual fee (growing annually with inflation).

The market potential for further growth is very strong, given that 1.2 million customers still need to install smart meters (Yu will account for just 2.4% of the market by the end of 2024).

Actively hiring

I was positively surprised by the amount of vacancies on Yu Energy's website, especially compared to its close peers. Yu has 28 open job positions (at the end of June), which is 9% of its total headcount.

Valuation

The stock trades at just a forward P/E of 9.1x. Adjusted for the net cash position, the stock is at 6.4x. I think there is scope for the company to earn more in 2024, given that its contracted revenue for 2024 is already £520mn (+111% higher YoY), and historically, Yu delivered 60% more sales than contracted for the period.

The company is guiding for 50% sales growth this year (vs. +111% higher contracted revenue) and a 6-8% mid-term EBITDA margin (vs. 9.3% in 2023). Assuming a moderate decline in energy prices, Yu could be on track to achieve close to £1bn revenue already in 2026 with an EBITDA of c. £70mn (7% margin).

At this profitability, it is currently valued at 3x EV/EBITDA (2026e).

Yu has introduced a progressive dividend policy with a payout ratio of 20-25%, but it plans to increase the payout to one-third of earnings.

Apart from low liquidity and the company flying below the radar for many investors, I think another reason for such an undemanding valuation is that the company’s sales correlate with energy tariffs. 2022-23 was a period of extraordinarily high energy prices, which are now declining. However, there is a limit to how much these prices can fall further as the price is usually set by gas as the marginal fuel. Importantly, Yu will likely offset softer prices by winning new customers and adding new services, as it has done historically.

There is also a political risk if the Labour government decides to introduce a cap on energy tariffs for SMEs (similar to residential supply).

Finally, Yu is exposed to the broader economy, as its customers could reduce energy consumption or even fail to pay the bills in a severe economic recession.

The company is guiding for 50% sales growth this year (vs. +111% higher contracted revenue) and a 6-8% mid-term EBITDA margin (vs. 9.3% in 2023). Assuming a moderate decline in energy prices, Yu could be on track to achieve close to £1bn revenue already in 2026 with an EBITDA of c. £70mn (7% margin).

At this profitability, it is currently valued at 3x EV/EBITDA (2026e).

Yu has introduced a progressive dividend policy with a payout ratio of 20-25%, but it plans to increase the payout to one-third of earnings.

Apart from low liquidity and the company flying below the radar for many investors, I think another reason for such an undemanding valuation is that the company’s sales correlate with energy tariffs. 2022-23 was a period of extraordinarily high energy prices, which are now declining. However, there is a limit to how much these prices can fall further as the price is usually set by gas as the marginal fuel. Importantly, Yu will likely offset softer prices by winning new customers and adding new services, as it has done historically.

There is also a political risk if the Labour government decides to introduce a cap on energy tariffs for SMEs (similar to residential supply).

Finally, Yu is exposed to the broader economy, as its customers could reduce energy consumption or even fail to pay the bills in a severe economic recession.

Useful links for further reading

- Corporate website: https://www.yugroupplc.com

- IR Section: https://www.yugroupplc.com/investors

- Annual Report (2023): open to view

- Latest IR Presentation: open to view

- AIM listing prospectus (2016): open here

Other four companies [Premium Content]

- A family-run industrial company trading at an over 50% discount to NAV that runs the largest copper mines, railway and infrastructure businesses and has a net cash position.

- Consumer goods company - family-run toy manufacturer, listed in HK, with 15% annual sales growth (10-year CAGR), a net cash position (43% of the market cap) that is trading at 2.9x P/E (2023)

- Two EM banks with 20%+ ROE and 10-20% compound earnings growth, trading at 3-4x P/E.

You can read the profiles of these companies and get full access to the archive by becoming a Premium Subscriber (€36/month or €360/year).

.

__