4 February 2023

During the past three quarters, there has been a few issues with CNX's operational results. Having reviewed them carefully, I concluded that the original thesis is not as strong and decided to sell a third of my position. I discuss a few of those issues including lower incremental production from new wells, rising drilling costs, falling reserves replacement ratio, possible peak in the quality of acreage, some inconsistencies in conference calls and others.

Content

- Incremental production from new wells

- Rising drilling costs

- Despite high reserves life, production is in decline

- Reserves Replacement Ratio (RRR) is rapidly falling

- Quality of acreage has peaked out

- Guidance / Conference calls

- Bright Spots

- Conclusion

Incremental production from new wells

My main concern is the ratio of new wells drilled vs incremental production. It has dropped quite considerably in the past 3 years, although I think it is mainly due to COVID, which led them to cut production in 2020.

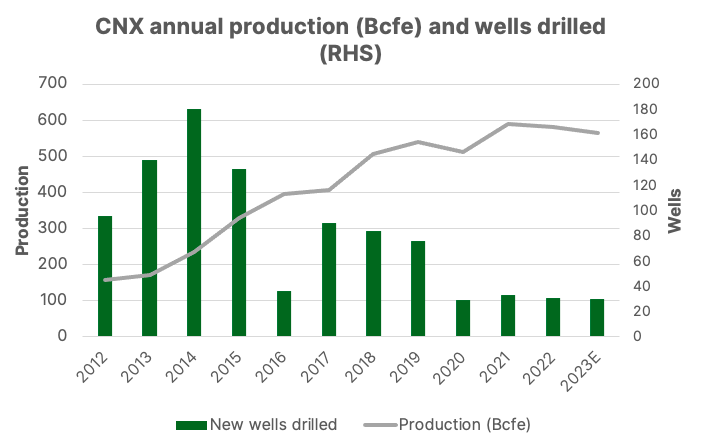

Looking at the 10+ years of historical production and drilling activity, you can first draw quite a positive conclusion. The company has reduced its drilling activity while simultaneously boosting its gas output. Indeed, during 2012-’14, CNX used to drill 140 wells per year, while production averaged 188 Bcfe. More recently, its drilling activity has reduced to just 31 wells a year (about one-fifth of the previous level), whereas gas output has increased to 578 Bcfe (3x increase).

Looking at the 10+ years of historical production and drilling activity, you can first draw quite a positive conclusion. The company has reduced its drilling activity while simultaneously boosting its gas output. Indeed, during 2012-’14, CNX used to drill 140 wells per year, while production averaged 188 Bcfe. More recently, its drilling activity has reduced to just 31 wells a year (about one-fifth of the previous level), whereas gas output has increased to 578 Bcfe (3x increase).

Source: Company data, Hidden Value Gems

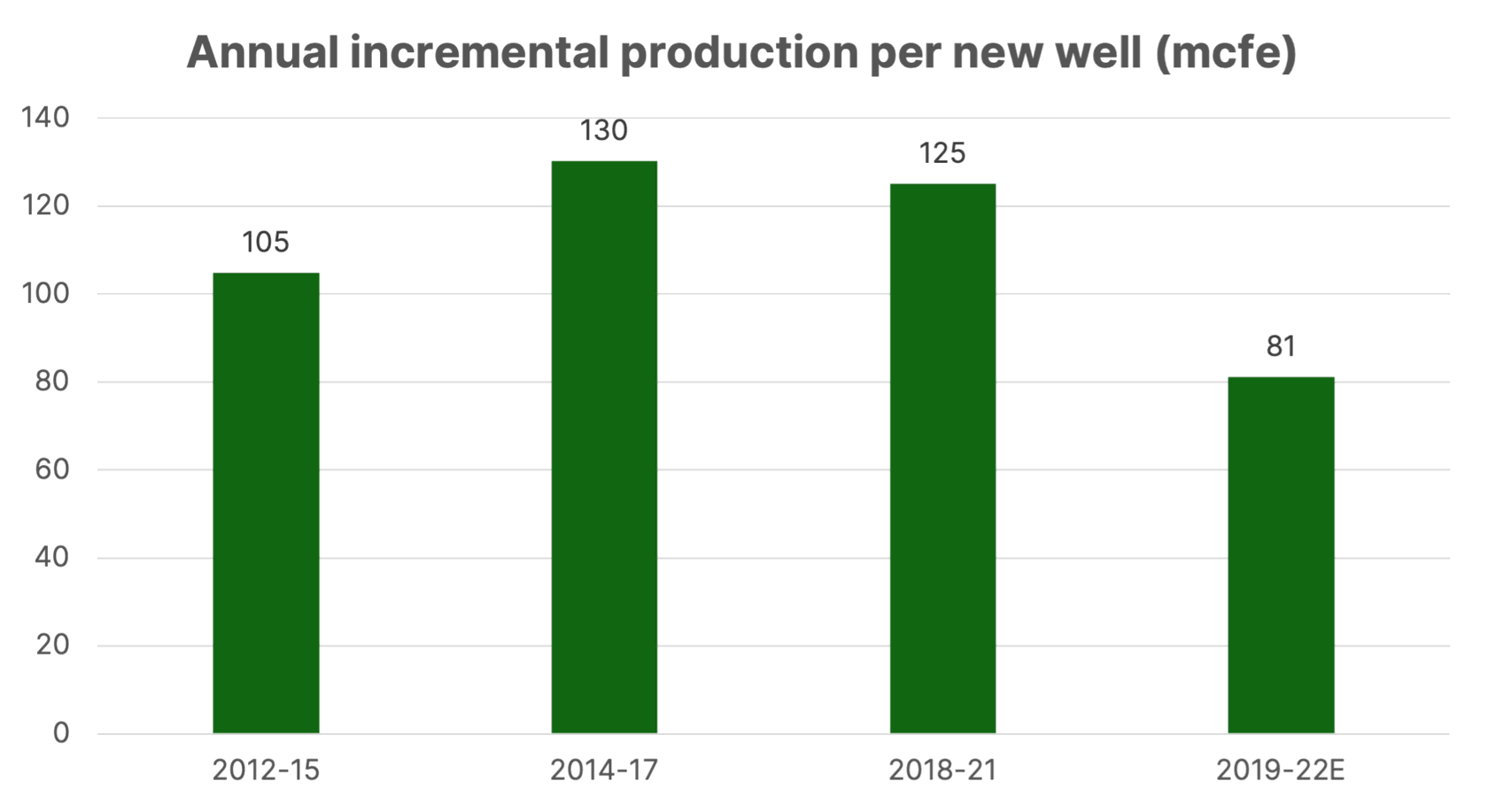

Incremental changes provide a completely different picture, however. I have calculated how much new wells contributed to the growth and used a 3-year average to smooth out volatility (a well can be drilled but not launched, or some wells may have been retired in the same year, or drilling could have been skewed towards the end of the year). As a disclaimer, I should flag that CNX has been active in M&A deals, especially in the past, mostly selling acreages, although it acquired new properties too. As a result, comparing different periods may only partially be accurate. Still, the big picture and the main conclusion should stay the same.

Source: Company data, Hidden Value Gems

In the past three years (2019-’22), one new well delivered only 81mcfe of additional production (on average), while it used to deliver 105-130mcfe in the past. It looks like 30 wells per year is barely enough to stem the decline. The risk is that with lower well productivity, CNX may need to drill more wells to keep production flat. If you add cost inflation, supply chain bottlenecks and potential technical failures (like the one which took place in Q3 2022), the situation starts to look more worrying.

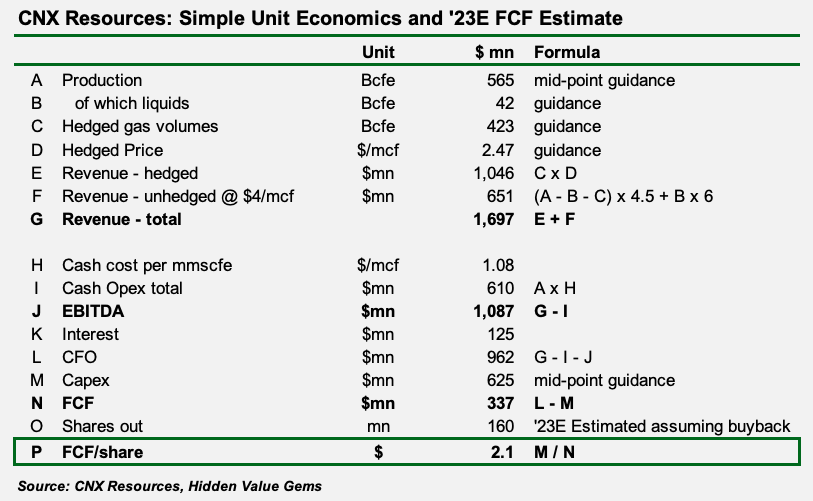

I think the chances that FCF will be squeezed (in a flat gas price environment) is quite high. I used to view $700mn annual FCF as a base case, but this is not the case any more.

I think the chances that FCF will be squeezed (in a flat gas price environment) is quite high. I used to view $700mn annual FCF as a base case, but this is not the case any more.

Rising drilling costs

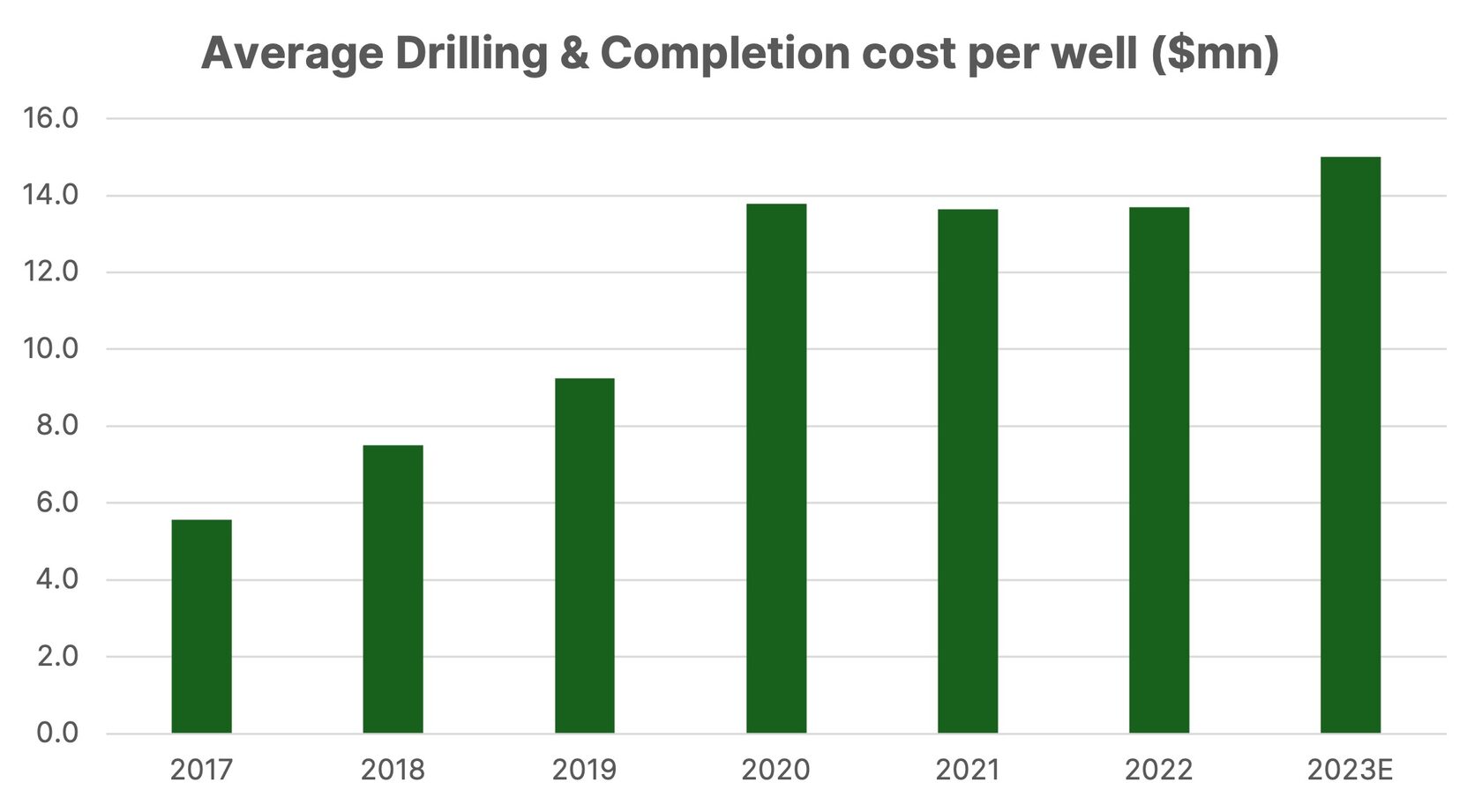

Based on 2023E guidance, CNX would spend about $15mn to drill and complete one well, compared to $5.6mn back in 2017. Inflation is cyclical, so extrapolating this trend would be wrong. However, equally misleading would be to use the metrics from 2017-2019 in the medium term.

Source: Company data, Hidden Value Gems

Despite high reserves life, production is in decline

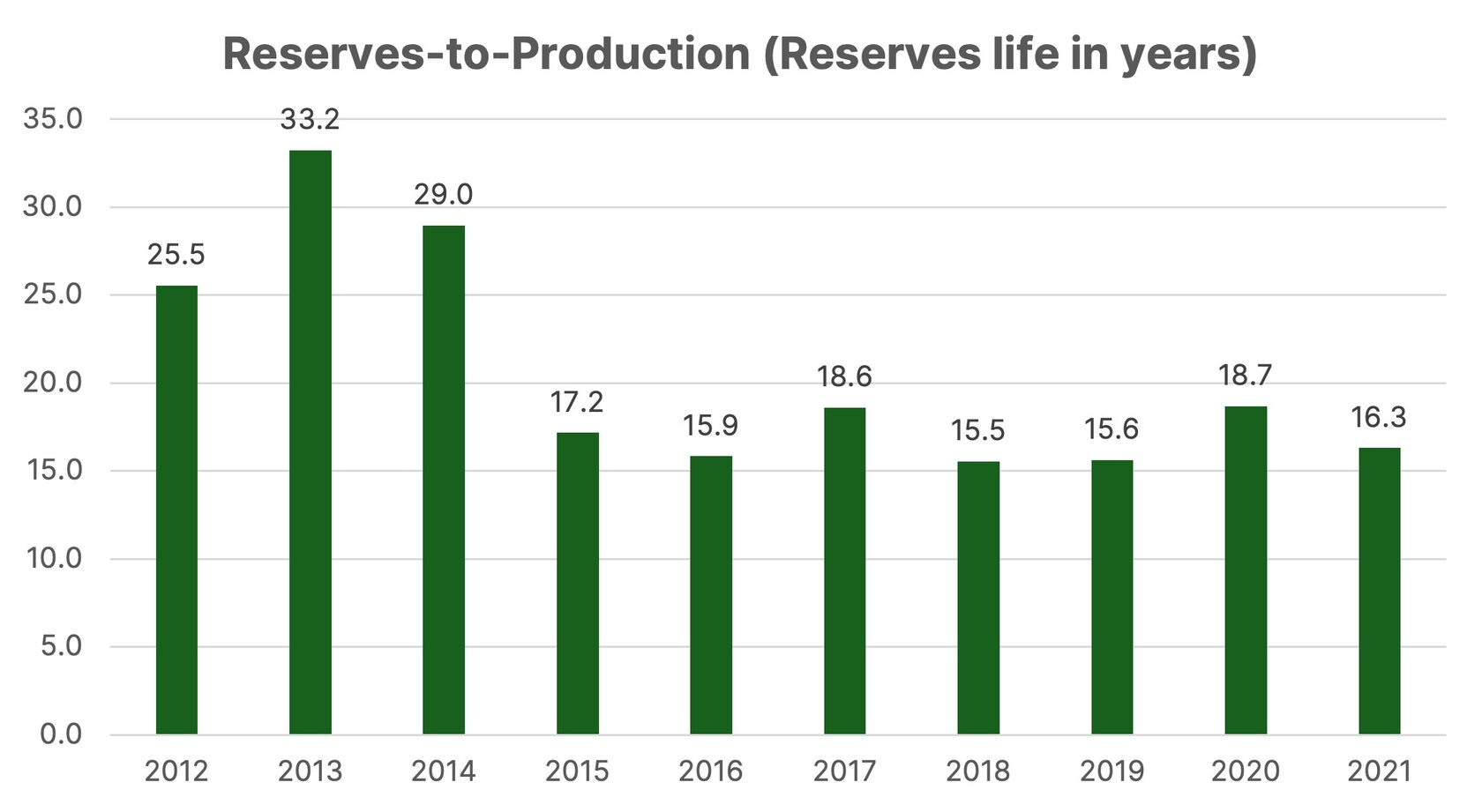

The usual rule of thumb in the oil & gas sector is to look at the ratio of proved reserves to annual production (also referred to as reserves life). The ratio at 10x or less suggests that the asset has entered a permanent decline with 10%+ (annually). A 20x ratio or high indicates that the asset is pretty young and has the potential for fast growth.

Source: Company data, Hidden Value Gems

CNX’s reserves life has been over 25 years 10 years ago but has since declined to 16. Not a dangerous level at all. However, what looks strange is that the company is not able to grow output despite its high reserves life. I understand it could be management’s choice to invest in its own shares rather than in new wells, but losing production when your ratio is relatively high looks odd. It might suggest that maybe the quality of reserves is not as high as the numbers suggest.

The unsuccessful well drilling in Q3 2022 gives further reasons for concerns.

The unsuccessful well drilling in Q3 2022 gives further reasons for concerns.

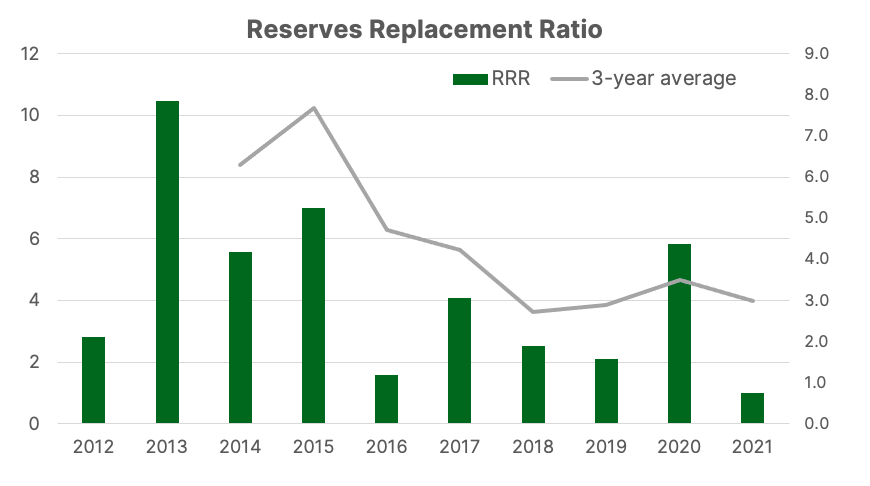

Reserves Replacement Ratio (RRR) is rapidly falling

More worrying is the declining RRR, which dropped to 1.0x in 2021. The ratio compares new reserves added through discoveries and extensions to annual production (hydrocarbons taken out of the ground). A ratio above one suggests that the firm increases its reserves base and can boost production in the future. If the ratio is below 1, then production decline is inevitable. Many companies try to mask the changes by acquiring new assets or changing assumptions about future costs to make reserves quantities less sensitive to price fluctuations. I have excluded reserves changes due to price changes and other non-organic factors (M&A).

Source: Company data, Hidden Value Gems

Given the decline in the ratio and weaker production despite the reserves life of 16 years, the new reserves estimates for 2022 will be of particular interest. They are usually published around mid-February. A significant decline in reserves would be an even more worrying signal.

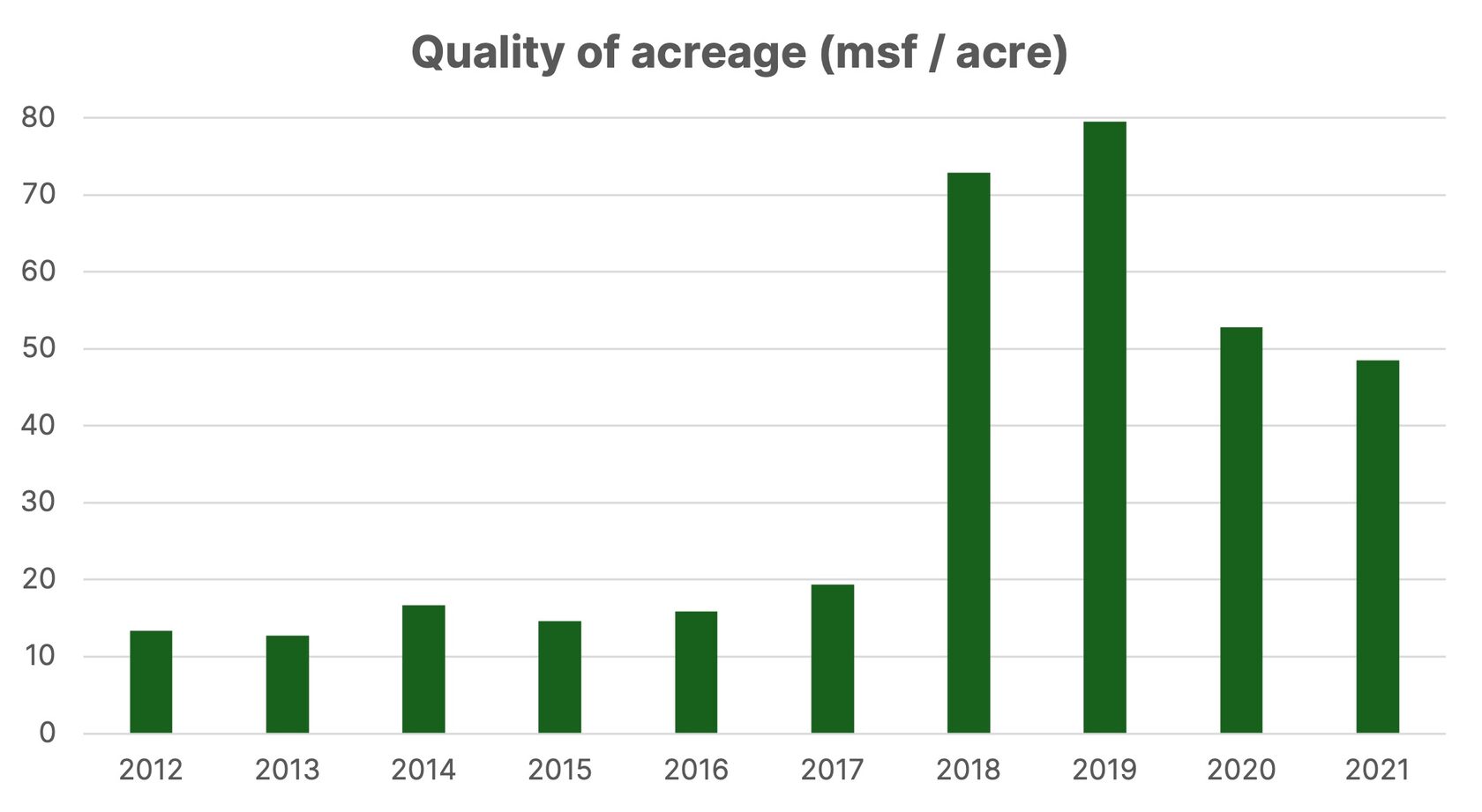

The quality of acreage has peaked out

The last data point which made me concerned about CNX’s asset quality is the amount of reserves per acre. CNX used to have large acreage with CBM reserves which I removed from my analysis. CBM (coal bed methane) is gas contained in coal mines.

Source: Company data, Hidden Value Gems

While the ratio has materially improved since 2012, the trend of the past three years has been negative. The amount of hydrocarbon reserves in one acre has dropped by 39%. As with the previous indicator, the data for 2022 will be critical to have more confidence in the conclusions.

Guidance / Conference calls

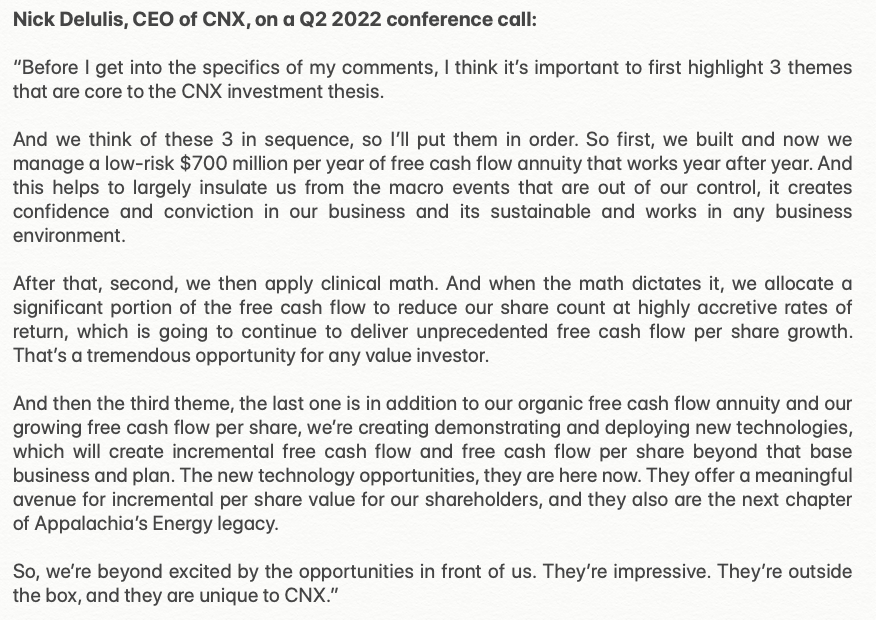

The message delivered by CNX’s management on their priorities and strategy is phenomenal. A simple ‘copy-paste’ of their shareholder letter or a regular conference call transcript could be easily used in the next book on value-based management and the creation of shareholder value. Consider this:

Source: CNX Resources

However, once you start tracking the messages from one call to another, you notice a few minor inconsistencies. Firstly, the FCF of $700mn (‘annuity’), mentioned during the Q2 2022 conference call, was then ‘downgraded’ to $500mn in the next call. During the Q4 2022 call, management provided new guidance for FCF in 2023 of $375mn.

Another issue I have is regarding production guidance and capex spending. Back in July 2022 (on a 2Q22 call), management explained the increase in capex plans for 2022 by bringing an additional drilling rig in the second half of the year (one of the key reasons). According to management, the rationale for doing so was to ‘de-risk’ their operations and add ‘optionality’ to increase capacity if they decide to do so.

However, fast forward to the next conference call (27 October 2022), and the management reduced its production target for 2022 by 5Bcfe (c. 1%), referring to the timing of wells completion as one of the reasons for lower output. Ok, maybe more wells were supposed to come online in late December 2022 with minimal contribution to 2022 production, but then 2023 production should benefit from more wells launched at the start of the period.

Unfortunately, this did not help—quite the opposite. During the latest call on 26 July 2023 (Q4 2022 results), management provided its 2023 production guidance of 565 Bcfe (mid-point of the guidance range), which implied a 2.6% production decline. Moreover, according to the company, the lowest production during the year is now expected to be during this quarter (Q1 2023). The company blamed operational delays and weather conditions.

To remind, CNX also encountered problems in Q3 2022 while drilling a vertical section at a Utica well. A formation above Utica started to break apart and became unstable. Various mitigation techniques did not help, and management decided to plug & abandon the well. Importantly, CNX stated that it ‘didn’t lose the reserves’ and that it had found necessary engineering solutions to drill those reserves later in the future.

While operational challenges happen in this business, I prefer management to be more realistic (and perhaps humble) about the prospects. Quite often, they discussed using one rig as the main advantage since it allowed the company to focus on and achieve higher efficiency instead of operating multiple rigs at various locations.

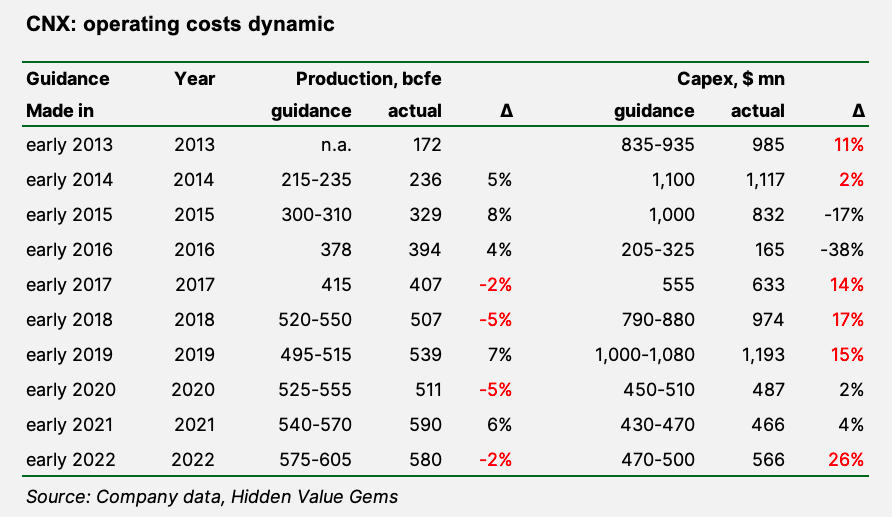

I have summarised the company’s initial guidance and actual results in the table below. In the past 10 years, CNX overspent on capex 60% of the time and underdelivered on production targets 40% of the time.

Another issue I have is regarding production guidance and capex spending. Back in July 2022 (on a 2Q22 call), management explained the increase in capex plans for 2022 by bringing an additional drilling rig in the second half of the year (one of the key reasons). According to management, the rationale for doing so was to ‘de-risk’ their operations and add ‘optionality’ to increase capacity if they decide to do so.

However, fast forward to the next conference call (27 October 2022), and the management reduced its production target for 2022 by 5Bcfe (c. 1%), referring to the timing of wells completion as one of the reasons for lower output. Ok, maybe more wells were supposed to come online in late December 2022 with minimal contribution to 2022 production, but then 2023 production should benefit from more wells launched at the start of the period.

Unfortunately, this did not help—quite the opposite. During the latest call on 26 July 2023 (Q4 2022 results), management provided its 2023 production guidance of 565 Bcfe (mid-point of the guidance range), which implied a 2.6% production decline. Moreover, according to the company, the lowest production during the year is now expected to be during this quarter (Q1 2023). The company blamed operational delays and weather conditions.

To remind, CNX also encountered problems in Q3 2022 while drilling a vertical section at a Utica well. A formation above Utica started to break apart and became unstable. Various mitigation techniques did not help, and management decided to plug & abandon the well. Importantly, CNX stated that it ‘didn’t lose the reserves’ and that it had found necessary engineering solutions to drill those reserves later in the future.

While operational challenges happen in this business, I prefer management to be more realistic (and perhaps humble) about the prospects. Quite often, they discussed using one rig as the main advantage since it allowed the company to focus on and achieve higher efficiency instead of operating multiple rigs at various locations.

I have summarised the company’s initial guidance and actual results in the table below. In the past 10 years, CNX overspent on capex 60% of the time and underdelivered on production targets 40% of the time.

The bright spots

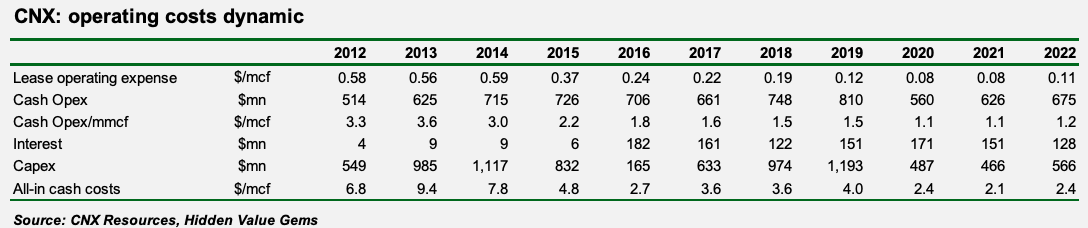

For a more well-rounded view, I have added other more positive points for consideration. In particular, it is worth highlighting the company’s good track in managing opex, which has declined by 65% to $1,2/mcf since 2012. Opex, however, started to rise in 2022 by 10% compared to 2021.

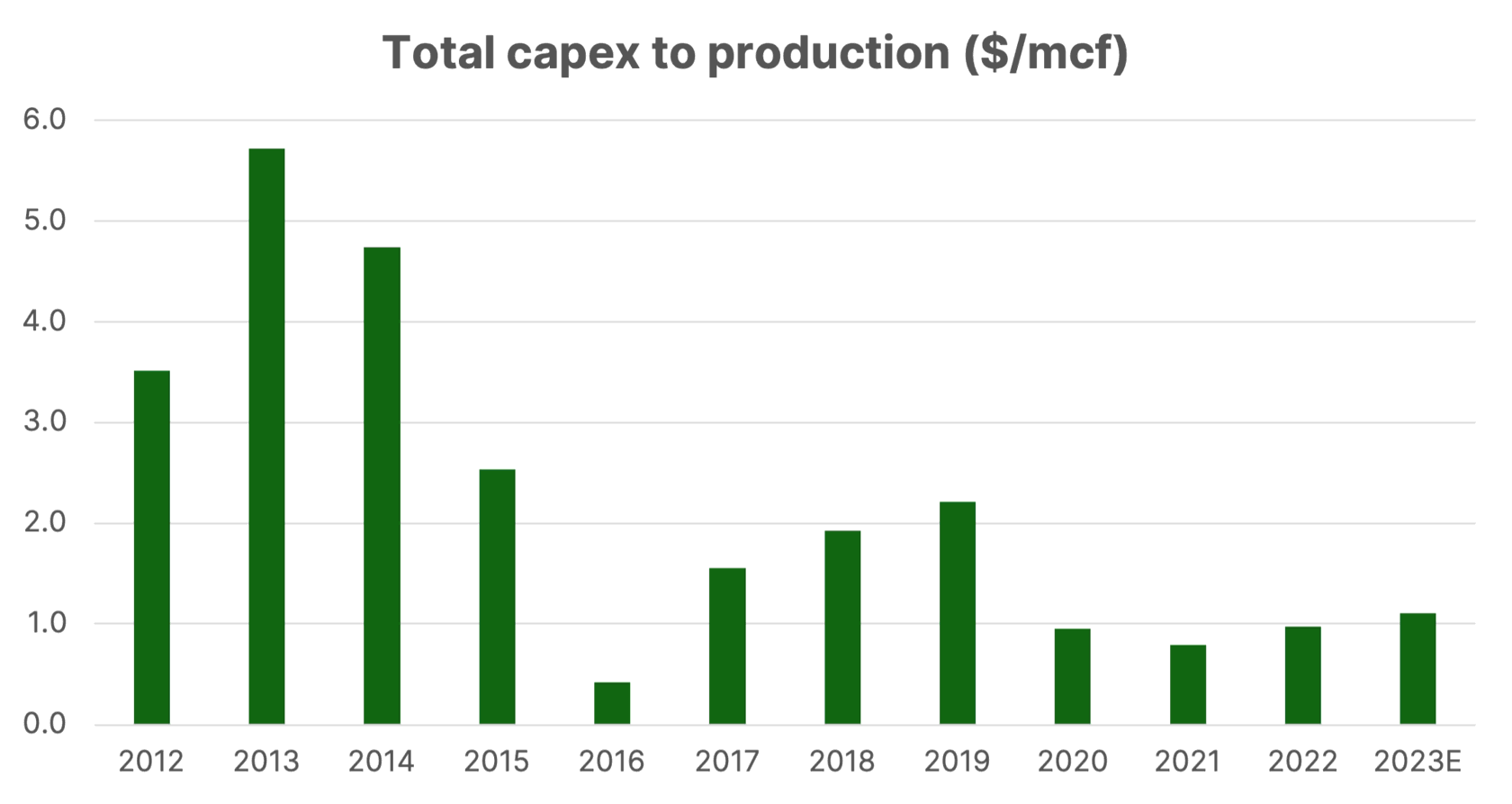

The company generally maintains high capex efficiency compared to its earlier years. Even with the new increased capex guidance for 2023 ($625mn, or 34% higher than in 2021), CNX spends $1 per one mcf of gas production now, compared to $3-5/mcf before 2015.

Source: Company data, Hidden Value Gems

I like that management of CNX has been consistent with its buyback programme. It spent $565.1mn on buyback in 2022 alone, reducing its share count by 16% in that period. However, repurchasing activity will gradually decline if FCF generation falls (as is the case for 2023).

Source: Company data, Hidden Value Gems

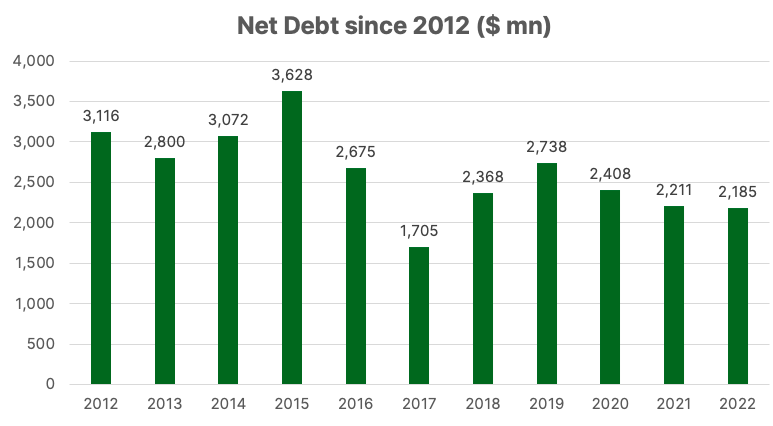

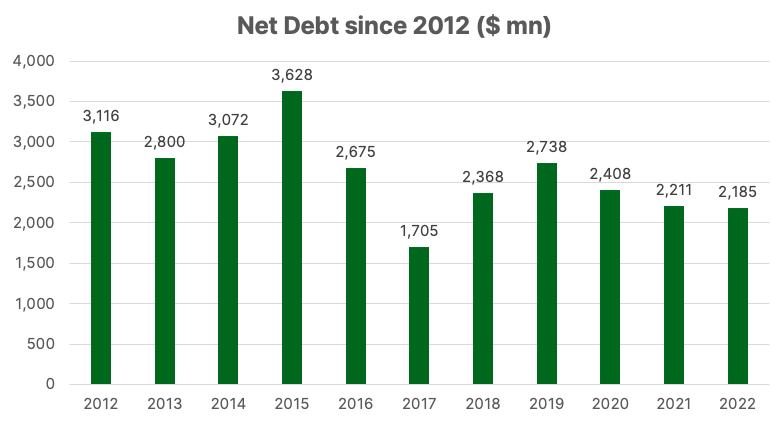

The company also reduced its net debt by 20% ($553mn) in the past three years to $2,185mn and by 30% ($931mn) since 2012, although as in the case of buyback it is really a function of FCF.

Source: Company data, Hidden Value Gems

The alignment of interests between top management and other shareholders is quite strong, which is another significant advantage of CNX. Key executives receive most of their compensation linked to the share price performance and FCF per share. They bought CNX shares at an open market a few years ago (at $7-10) and have yet to sell. The last reported share sales took place in the 2013-2014 period in the $30-40 price range.

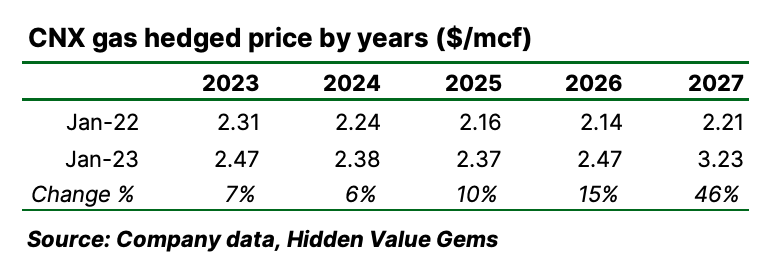

Finally, it is worth mentioning that the company has improved its gas hedging over the past year by locking in 10%+ better prices in the future years (see below).

Finally, it is worth mentioning that the company has improved its gas hedging over the past year by locking in 10%+ better prices in the future years (see below).

Conclusion

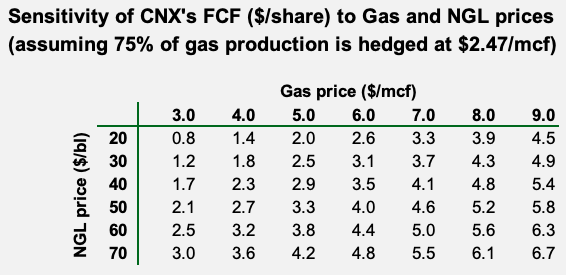

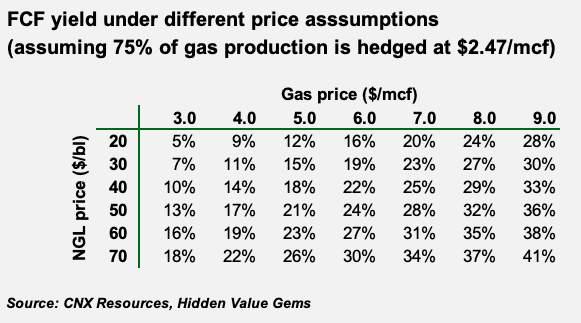

The main conclusion from closely following the company over the past six months is that its asset quality is lower than I initially thought. Reserves do not support easy production growth, and even maintaining flat output requires more than I originally estimated. As a result, the normalised FCF of CNX is well below $700mn, closer to the $300-400mn range. This translates into an 11-15% FCF yield.

This FCF yield needs to be adjusted for the future tax rate (20%), which the company will start paying after its cumulative FCF exceeds $3bn (from 2020), which should happen at some point after 2025. Besides, as a commodity producer, CNX cannot maintain output indefinitely and, at some point, will face a sharp decline in volumes. In other words, the same FCF yield offered by a manufacturing company that does not face the same depletion problem is more attractive.

As a small side note, when the management of CNX reports its FCF numbers, it includes proceeds from asset sales (acreage, which it deems to be of low interest to CNX). As a result, FCF reported by the company often exceeds my estimates which are based on a simple difference between cash flow from operations and capex.

As a small side note, when the management of CNX reports its FCF numbers, it includes proceeds from asset sales (acreage, which it deems to be of low interest to CNX). As a result, FCF reported by the company often exceeds my estimates which are based on a simple difference between cash flow from operations and capex.

As the valuation is less attractive than I thought initially, and there are a few questions about the quality of the company's reserves base, I have decided to sell a third of my position at around $15.75. I think the company should maintain a 10%+ annual buyback rate, and with high insider ownership, the stock has limited downside risks. I plan to reduce my position further, closer to $20, assuming no major news/changes to the investment case in the meantime.

I would like to finish this update by thanking my subscribers for taking the time to read the notes and occasionally providing invaluable feedback. In the case of CNX, I am particularly grateful to the subscriber from the UK who has asked me a few questions on the quality of CNX's reserves and has pointed to some additional materials (here and here). This triggered me to question my original assumptions and eventually led to a better understanding of the company. Meeting like-minded investors, even via email, is one of the reasons I have launched this blog.

DISCLAIMER: This publication is not investment advice. The primary purpose of this publication is to inform and educate readers about the stock market. Readers should do their own research before making decisions and always consult with professional advisors. Information provided here may have become outdated by the time you read it. All content in this document is subject to the copyright of Hidden Value Gems. Please read the full version of the Disclaimer here.